Trending

This story is from August 19, 2019

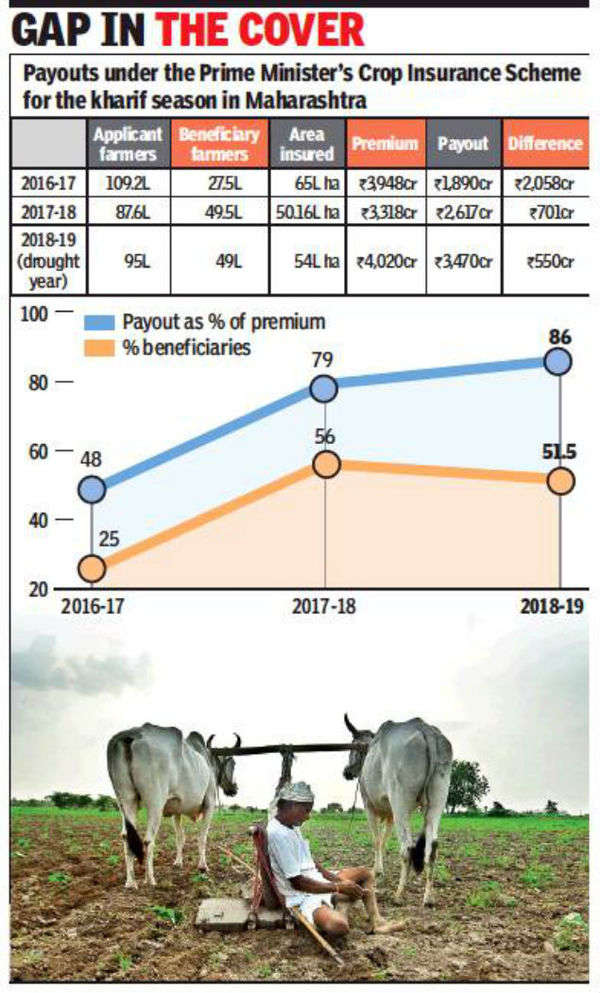

Maharashtra: Even in drought year, premiums more than insurance payouts to farmers

Premium paid to insurance companies has outstripped compensation to farmers during the kharif season in all three years of the Prime Ministers Crop Insurance scheme (PMFBY) in Maharashtra, latest data shows. This was true even for 2018-19—a drought year with over 40% of the state’s talukas affected by a water crisis.

The number of farmers compensated for the 2018-19 kharif season is 49 lakh, almost on par with 49.5 lakh who got compensation for crop losses in the same period of the previous year

MUMBAI: Premium paid to insurance companies has outstripped compensation to farmers during the kharif season in all three years of the Prime Ministers Crop Insurance scheme (PMFBY) in Maharashtra, latest data shows. This was true even for 2018-19—a drought year with over 40% of the state’s talukas affected by a water crisis.

Premium paid to insurance companies in kharif season over the past three years totalled Rs 11,286 crore while compensation paid to farmers for crop losses was Rs 7,977 crore.This is a difference of Rs 3,309 crore. Kharif, sown during monsoon, is the main crop in Maharashtra. In the kharif season of the drought year of 2018-19, there was a gap of Rs 550 crore between the premium paid to insurance companies and payout to farmers. Premium paid to insurance companies was Rs 4,020 crore and compensation paid to farmers Rs 3,470 crore.

The number of farmers compensated for the 2018-19 kharif season is 49 lakh, almost on par with 49.5 lakh who got compensation for crop losses in the same period of the previous year. Only 51.5% of the farmers who applied for crop insurance were compensated for the ’ 18-19 kharif season.

Critics such as Marathwada-based activist Rajan Kshirsagar, though, say the very design of the scheme goes against farmer interests. “Insurance companies are getting huge premiums from the government but the bulk of insurance claims from farmers are rejected,” he alleged.

The scheme follows an area-based approach, and the unit considered in the state is a revenue circle. “In order to qualify for compensation, the farmer will have to report a yield which is less than the average yield of the revenue circle. So, if an individual farmer has suffered losses but the yield of a revenue circle is high, it is difficult for him to get compensation,” said Kshirsagar.

Officials say both the state and insurers take a higher risk under the PMFBY. “In the earlier National Agriculture Insurance Scheme (NAIS), the insurance company’s liability was capped at the amount of premium. Under PMFBY, the payout is capped at 350% of premium,” said one. Under NAIS, a farmer paid the premium. Under PMFBY, a farmer pays 1.5% of the sum insured for kharif crop and 2% for rabi. The remaining premium is equally divided between the Centre and the state. Officials say premiums are bound to be higher than payouts in a good year. “After all, insurance payouts will be high only when there is crop loss.”

Meanwhile, a public sector insurance company official said crop insurance is in the nature of a catastrophe cover. A period of a year or two cannot be used to determine the experience. “Premium has been scientifically calculated taking into account possibility of crop failure and its impact. When there are claims, they occur across a whole region. As these are low-frequency events, claims cannot be revised annually.”

Premium paid to insurance companies in kharif season over the past three years totalled Rs 11,286 crore while compensation paid to farmers for crop losses was Rs 7,977 crore.This is a difference of Rs 3,309 crore. Kharif, sown during monsoon, is the main crop in Maharashtra. In the kharif season of the drought year of 2018-19, there was a gap of Rs 550 crore between the premium paid to insurance companies and payout to farmers. Premium paid to insurance companies was Rs 4,020 crore and compensation paid to farmers Rs 3,470 crore.

The number of farmers compensated for the 2018-19 kharif season is 49 lakh, almost on par with 49.5 lakh who got compensation for crop losses in the same period of the previous year. Only 51.5% of the farmers who applied for crop insurance were compensated for the ’ 18-19 kharif season.

Officials, though, say the state has fared well under PMFBY. “Although there was a drought in 2018-19, the rabi season was affected much more than kharif. During the kharif season, both sowing and productivity were high. Those who suffered crop losses received insurance,” said state agriculture secretary Eknath Davale. He said the percentage of compensation paid to farmers as a share of premiums has improved post the scheme’s 2016 launch.

Critics such as Marathwada-based activist Rajan Kshirsagar, though, say the very design of the scheme goes against farmer interests. “Insurance companies are getting huge premiums from the government but the bulk of insurance claims from farmers are rejected,” he alleged.

The scheme follows an area-based approach, and the unit considered in the state is a revenue circle. “In order to qualify for compensation, the farmer will have to report a yield which is less than the average yield of the revenue circle. So, if an individual farmer has suffered losses but the yield of a revenue circle is high, it is difficult for him to get compensation,” said Kshirsagar.

Officials say both the state and insurers take a higher risk under the PMFBY. “In the earlier National Agriculture Insurance Scheme (NAIS), the insurance company’s liability was capped at the amount of premium. Under PMFBY, the payout is capped at 350% of premium,” said one. Under NAIS, a farmer paid the premium. Under PMFBY, a farmer pays 1.5% of the sum insured for kharif crop and 2% for rabi. The remaining premium is equally divided between the Centre and the state. Officials say premiums are bound to be higher than payouts in a good year. “After all, insurance payouts will be high only when there is crop loss.”

Meanwhile, a public sector insurance company official said crop insurance is in the nature of a catastrophe cover. A period of a year or two cannot be used to determine the experience. “Premium has been scientifically calculated taking into account possibility of crop failure and its impact. When there are claims, they occur across a whole region. As these are low-frequency events, claims cannot be revised annually.”

End of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In City

Entire Website

- Israeli missiles hit site in Iran, explosions heard at airport: Key points

- JAC 10th Results 2024 Live: Jharkhand board Matric result today on jacresults.com

- IPL Today Match LSG vs CSK: Dream11 prediction, head-to-head stats, fantasy prediction, key players, pitch report and ground stats of IPL 2024

- Meet Vasuki Indicus, the ‘crocodile’ that was a 50ft snake

- Maharashtra speaker Rahul Narwekar creates stir in BJP, says he’s in don Arun Gawli’s gang now

- Apple iPhone 13 available for just Rs 15,336 on Amazon; check out the offer details

- Best 75 inch Smart TVs in India: Top Picks For A Premium Viewing Experience

- LSG vs CSK: Is Mayank Yadav fit to have a go at MS Dhoni & Co? Here's an update

- Watch - 'Isiliye tika laga ke aya': When Shardul Thakur missed wishing KL Rahul 'Happy Birthday'

- Indian runner Shalu Chaudhary cleared of doping charges; NADA ordered to refund Rs 1.5 lakh within ten days

- Bullet to ballot: Manipur begins uneasy journey as voting under way in phase 1 of LS polls

- Iran shuts airspace, halts flights after Israel's retaliatory attack

- Is a weaker rupee a sign of a weak Indian economy?

- Kejriwal's health in spotlight as AAP, ED clash over mangoes

- Israel-Iran war: 'Send rockets not at each other but..', says Musk

- 'Woman wearing only undergarments just boarded our bus'

- From #236 to #1, the story of IAS toppers’ giant leap

- Read TCS CEO's ‘thanks letter’ to employees and COO

- Congress like 'Mahabharata’s Shalyya': FM Nirmala

- TN polls: 23.8% voter turnout by 11 am

Popular Categories

Hot on the Web

Top Trends

Jasprit BumrahArvind KejriwalJAC 10th ResultTamil Nadu Lok Sabha ElectionIsrael Iran War NewsLok Sabha Election Phase 1IPL Today MatchStock MarketIPL Live ScoreBest AC Brands in IndiaIPL Orange Cap 2024IPL Purple Cap 2024IPL 2024 ScheduleLok Sabha Election Full ScheduleIPL Points TableIPL Match Full Schedule

Trending Topics

Bade Miyan Chote Miyan CollectionAR RahmanDeepika PadukoneBalram Mattannur Death NewsRam Temples In IndiaDubai FloodSamarth JurelRam Lalla OutfitAnushka SharmaMasaba Gupta Pregnancy NewsShilpa ShettyJennifer Mistry Bansiwal Sister DeathDibakar BanerjeeArticle 370 OTT ReleaseHappy Relationship TipsNita AmbaniBest 1000 Litre Water TankBest Dishwashers In IndiaBest 75 Inch Smart TvBest Inverters For Homes

Living and entertainment

Latest News

iPhone 17 Plus to be less ‘plus’ in terms of display, here’s what’s changingLok Sabha elections 2024 full schedule: Bengaluru to vote in phase 2 on April 25Taarak Mehta Ka Ooltah Chashmah update, April 18: Gokuldham wasis perform Ram Navmi pujaTaapsee Pannu praises Ajay Devgn's 'Maidaan's and indirectly condemns its dull box office response, 'Then Let's Not Say Our Big Films Lack Soul'IPL 2024: Harbhajan Singh hails Ashutosh Sharma for 'winning hearts'Bhagiratha beneficiaries, tribals dig pits for waterRupanjana Maitra to tie the knot with Ratool Mukherjee todayNASA discovers a hidden galaxy containing 'billions of stars'Madhya Pradesh first phase polls: 30.46% voter turnout till 11amSatellite phones make a debut in this Bengal electionIIT Kanpur is shaping India’s future FinTech leaders with its e-Masters Degree Programme in Financial Technology & ManagementEnnore villagers withdraw resolution to boycott pollsFM Nirmala Sitharaman’s sharp barb: Congress like 'Mahabharata’s Shalyya', keeps saying India can’t match ChinaParc Jae Jung reveals enlistment date alongside upcoming song releaseRebecca Wisocky delves into Hetty's heartbreaking revelation in 'Ghosts Season 3'Women to manage all polling stations in MaheJharkhand Board 10th Result 2024 declared, direct link to download nowSalman Khan travels to Dubai with heightened security following shooting incident

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service